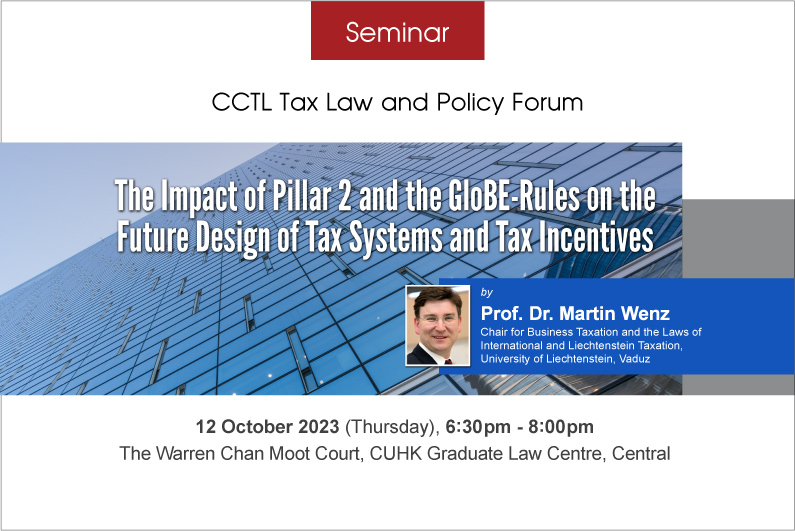

The global level-playing field on taxation as well as the tax systems of jurisdictions are currently challenged and amended essentially by the implementation of Pillar 2 and the GloBE-Rules regarding the global minimum taxation of 15% on certain multinational enterprises, wealth structures and family offices to floor tax competition. Alternatively, the US still follow their amended GILTI-Rules and address the implementation of certain GloBE-Rules as a refusable extraterritorial taxation. The seminar focuses on the tremendous impact of GloBE on the future design of tax systems and tax incentives post BEPS 1.0 and 2.0. In jurisdictions with a territorial tax system, a competitive tax burden or various preferential tax regimes like in Hong Kong, Ireland, Liechtenstein, Singapore, and Switzerland, traditional income- and expenditure-based tax incentives like IP-Boxes and R&D-super-deductions with reduced effective tax rates are mostly cancelled-out by GloBE-top-up taxes, subject to the introduction of so-called Qualified Refundable Tax Credits (QRTC). Vice versa, high tax countries like France, Spain and the UK still may use several traditional tax incentives like IP-Boxes and R&D-super-deductions with reduced effective tax rates in order to increase their tax competitiveness and to lower their effective tax burden even up to a maximum of 15%. Whereas tax competition in the past boosted cross-border BEPS and the respective use of tax incentives in highly competitive jurisdictions, the introduction of GloBE will support domestic BEPS measures to achieve a similar level of tax competitiveness in less competitive countries. Thus, tax competition is everything, but ended by the introduction of GloBE-Rules, and supplemented more and more by subsidy competition.

This seminar is jointly co-organized by the CCTL Tax Law and Policy Forum and International Fiscal Association – HK Branch.

About the Speaker:

Professor Dr Martin Wenz is a Professor of National and International Tax Law and holds the Chair for Business Taxation and the Laws of International and Liechtenstein Taxation at the University of Liechtenstein. He is also the Academic Head of the Liechtenstein Executive School and the Program Director of the Master of Laws (LL.M.) in International Taxation. His main research interests are the international tax policy, the re-design of tax systems, international tax standards, the international Level-playing-field on taxation, the international tax treatment of individuals, companies, private and charitable asset and wealth structures and the various aspects of the Liechtenstein tax law. Professor Wenz gives also comprehensive advice to the Liechtenstein Government on national and international tax law including Double Tax Agreements and on the Implementation of International and European Tax Standards including Pillar 2.

0 Comments